Imagine a world where a single flower bulb—not a house, not a ship, but a humble bulb destined for a garden—could be worth more than ten years of a skilled craftsman’s salary. This wasn’t a flight of fantasy; it was the reality of the Dutch Republic in the 1630s. In one of history’s most bizarre and dramatic financial episodes, the Netherlands was gripped by “Tulip Mania”, a speculative frenzy that serves as the quintessential cautionary tale of a market bubble and its inevitable, catastrophic pop.

A Golden Age and an Exotic Flower

To understand how a flower could bring an economy to its knees, we must first look at the setting: the Dutch Republic in the early 17th century. This was the Dutch Golden Age, a period of unprecedented prosperity. Fueled by global trade through corporations like the Dutch East India Company (VOC), wealth poured into cities like Amsterdam and Haarlem. Art, science, and commerce flourished. The newly rich merchant class, eager to display their status, developed a taste for luxury, art, and rare collectibles.

Into this wealthy, status-conscious society came the tulip. Originally a wildflower from the mountains of Central Asia, it had been cultivated and celebrated in the Ottoman Empire. In the late 1500s, the tulip was introduced to Europe, and the Dutch, with their horticultural skills and passion for novelty, fell in love. Its intense, pure colors were unlike anything seen in European gardens before, and the flower quickly became a must-have item for the elite.

From Garden Gem to Speculative Frenzy

What turned a simple passion for gardening into a speculative mania? The answer lies in a peculiar viral infection. Certain tulip bulbs were infected with the mosaic virus, which, rather than killing the plant, caused the petals to “break” into stunning, unpredictable patterns of flames and feathers. These “broken” bulbs were incredibly rare and beautiful, and they could not be reliably reproduced. A plain red tulip might, one year, produce a gloriously striped offspring, but there was no telling if or when it would happen.

This rarity made certain varieties, with evocative names like Viceroy and the legendary Semper Augustus (Always August), the ultimate status symbols. At first, the trade was confined to wealthy connoisseurs and botanists. But as stories spread of the immense profits being made, the market began to attract a wider array of people. Merchants, shopkeepers, and even common artisans saw tulips not as flowers to be planted, but as assets to be flipped for a quick profit.

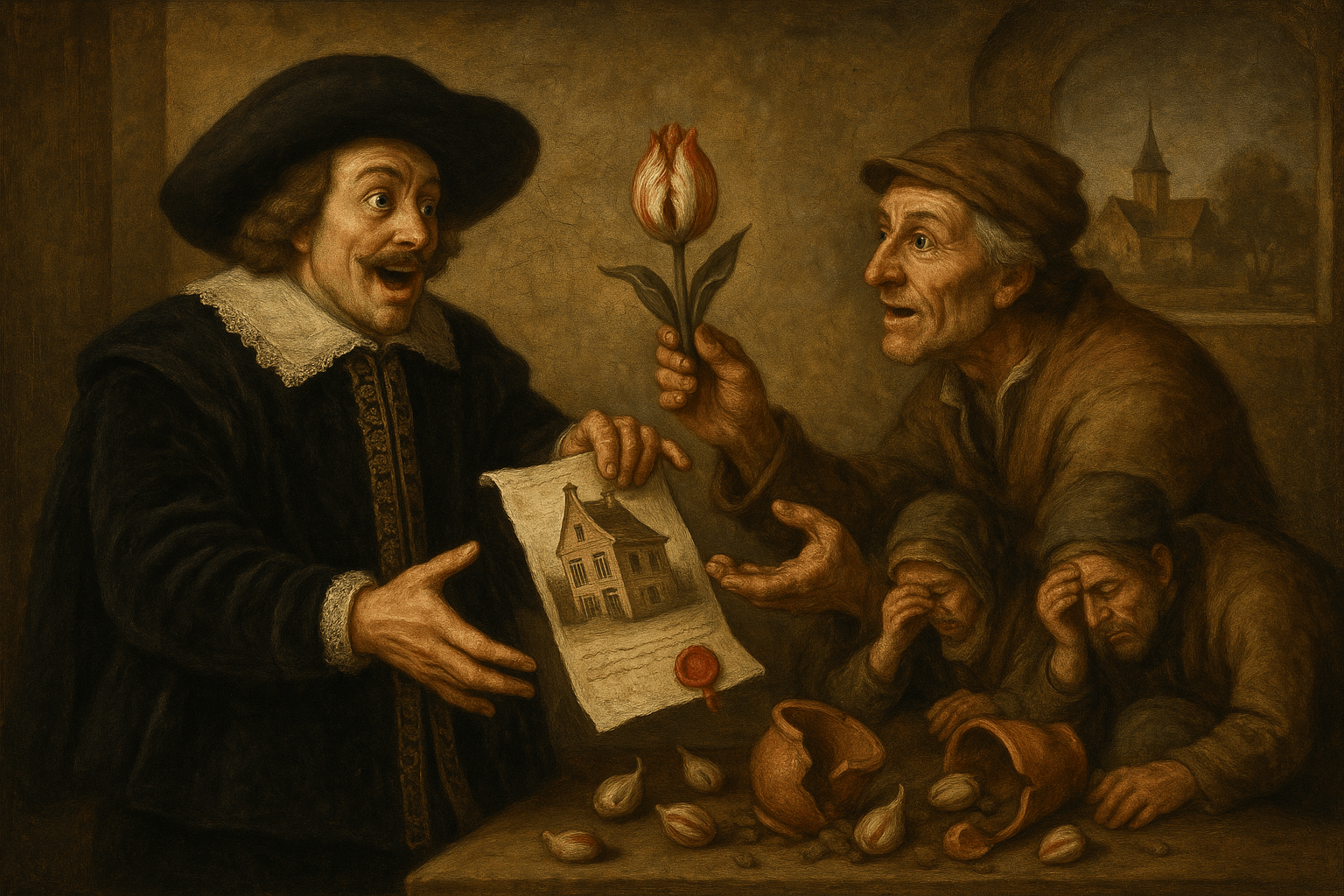

The Birth of a Bubble: Windhandel and Futures Markets

The speculative frenzy truly ignited with the development of a rudimentary futures market. Because tulip bulbs can only be moved during their dormant season in the summer, trading during the winter was impossible. To get around this, speculators began trading promissory notes for bulbs that were still in the ground. This practice became known as windhandel—literally, “wind trade”—because no physical goods were being exchanged, only the paper contracts for them.

This innovation detached the price of tulips from their physical reality. A single contract could be bought and sold multiple times before the bulb was ever due to be delivered. Trading often took place in taverns, where groups of men, fueled by beer and social pressure, would bid prices up to astonishing heights. By the winter of 1636, tulip speculation was the talk of the nation.

The prices reached absurd levels. While a common bulb might sell for a few guilders, the rare varieties commanded kingly ransoms. In one famous account, a single Viceroy bulb was reportedly traded for a small fortune’s worth of goods:

- Two lasts of wheat

- Four lasts of rye

- Four fat oxen

- Eight fat swine

- Twelve fat sheep

- Two hogsheads of wine

- Four tons of beer

- Two tons of butter

- 1,000 pounds of cheese

- A complete bed

- A suit of clothes

- A silver drinking cup

The most prized bulb of all, the Semper Augustus, could sell for 5,000 to 10,000 guilders—enough to purchase a grand canal house in Amsterdam.

The Inevitable Pop

For a bubble to sustain itself, there must always be a “greater fool” willing to pay an even higher price. In early February 1637, the Dutch ran out of fools. The catalyst was a routine bulb auction in the city of Haarlem. For the first time, buyers failed to show up and bid the expected high prices. Some speculators, perhaps sensing the market had reached an unsustainable peak, tried to cash out.

The news spread like wildfire. A flicker of doubt turned into full-blown panic. Everyone rushed to sell, but there were no buyers. Prices plummeted by over 90% within weeks. A bulb that had been “worth” 5,000 guilders was now worth 50, if a buyer could be found at all. Speculators who had promised to pay extravagant sums for bulbs were now facing financial ruin. They held contracts for worthless flowers and had no way to pay. The windhandel had blown itself out.

The Aftermath and Lasting Legacy

The crash created chaos. Contract holders defaulted en masse. For months, buyers and sellers argued in courts and town halls over who owed what. In the end, the Dutch government, viewing the contracts as gambling debts, offered a compromise: buyers could void their contracts by paying a small percentage of the agreed-upon price. This helped avert total-system collapse, but countless individuals were still financially ruined.

Some modern historians, like Anne Goldgar in her book Tulipmania, argue that the popular story has been exaggerated and that the economic devastation was not as widespread as legend suggests. The mania, she contends, was largely confined to a network of wealthy merchants and driven speculators, not the entire populace. However, there is no denying that for those involved, the crash was devastating.

Regardless of its exact scale, Tulip Mania entered history as the archetypal example of a speculative bubble. It perfectly illustrates how an asset’s price can become dangerously detached from its intrinsic value, driven instead by human greed, hope, and the madness of crowds. More than just a story about flowers, it’s a timeless lesson in market psychology that has echoed through every major financial bubble since, from the South Sea Bubble of the 18th century to the dot-com boom of the 1990s and the cryptocurrency manias of today. The Dutch may have eventually tired of paying a fortune for tulips, but humanity, it seems, has never lost its appetite for a bubble.